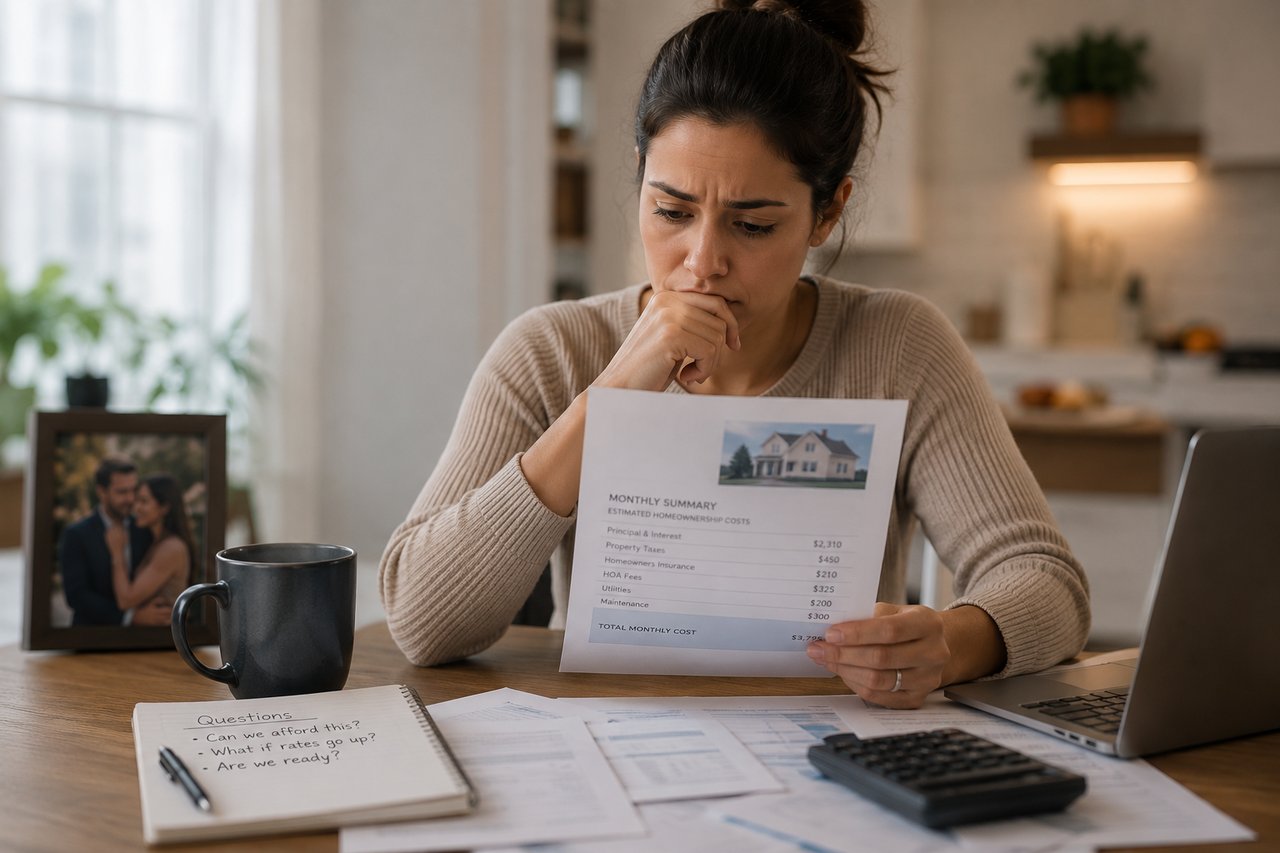

Negotiating your closing costs prior to buying a house can help you save money. How can you tell which closing costs are negotiable and which ones cannot?

The average closing cost ranges between 2% to 5% of the loan amount. It can be a large portion of your mortgage expenses.

A mortgage broker will give you a breakdown of closing costs as well as tips for how to get the lowest fees.

Are Closing Costs Negotiable

Closing costs These are fees charged by third-party lenders and mortgage brokers to help you obtain a mortgage and buy your home.

Banks, title companies, and government agencies require many services during closing. These services include reviewing and drafting loan documents and updating official records. They also review credit profiles and broker your loan or home sale.

All costs cannot be reduced. All fees charged by government agencies, including recording fees and title transfer fees are fixed. You will not be able to negotiate any third-party service with your lender.

This means you won’t have the ability to negotiate credit report fees, flood determination fees, or appraisal costs. On page 2, your loan estimate will include information about “services you cannot shop for”.

There are many options to obtain a better mortgage. Start by negotiating lower interest rates, discount factors, and origination fees. Negotiating can help to reduce these fees.

Title insurance, home inspections, and other settlement costs such as closing attorney fees are often eligible for discounts. These fees are generally less than origination fees but can add up over time.

The Consumer Financial Protection Bureau (CFPB) has revealed that consumers who shop around for closing costs can save up $500 on title services.

The National Average Homeowner’s Insurance Policy Is $1,083 Per Year

When you get a mortgage, homeowners insurance must be purchased. Bundle homeowners and auto insurance for the best rates.The average cost of homeowners insurance in the United States was $1,083. This is one of the few fees that buyers can control.

It is smart to compare quotes from different insurance companies in order to get the best home insurance rates.

Title Insurance Fees – 500 to $1,500

To buy a house, you must have a clean title. This ensures that your house is protected from any legal claims. To buy a house, you will need to hire someone to do title research and to purchase title insurance from lenders.While you’ll need to pay more upfront for points (and get lower interest rates and monthly payments), the cost of these points will be lower. The rate reduction per point is subject to change. Different lenders may offer different rates.

Lender credits are also available. These are the exact opposite of discount points. The mortgage broker credit reduces your upfront closing costs and allows you to obtain a higher interest rate on your mortgage.

You can adjust your mortgage terms by using the discount points and credit points of Mortgage Brokers. Keep in mind, however, that upfront costs can be exchanged for interest rate concessions.

Loan Origination Fees — 1% of the Loan Amount

These fees may be referred to by different names by lenders. These fees are part of the underwriting process.One lender may consider an application fee or underwriting fee to be an origination fee. It could be called an origination or rate-lock fee by another lender.

It doesn’t matter what the charge is called, it typically costs about 1% of your loan amount. This cost may vary from one lender to the next. The loan origination charge is found in the upper left corner of the second page of the loan estimate.

Mortgage Brokers will give you a loan estimate once you have applied for a loan. It is a smart idea to get multiple loan estimates from different lenders in order to ensure you get the best deal.

Real Estate Agents Commissions — 6% of the Purchase Price

Most residential real estate transactions involve both the buyer and seller’s agents. The money needed to pay a real estate agent is not required by homebuyers.The listing agent is usually paid out of the sale proceeds.

Each agent will receive 6% as a commission. The going rate will depend on the local market. Ask your agent for specific details.

How to Negotiate Your Closing Costs

Do not assume that the lender will give you the best loan deal when you apply. You might get a poor deal if you don’t negotiate. These are some tips to help you improve your negotiation skills.Before You Make an Offer

Before you make an offer, compare rates from different lenders. By shopping early, you can get information about closing costs and rates from several Beverly Hills Mortgage brokers. These details will be your advantage in negotiating every aspect of the loan.While you shop for mortgage brokers, let them know that you are searching for the best rates, and also consider closing costs. Ask your mortgage officer if the Mortgage Brokers offer rate matching guarantees or other flexible pricing options.

At this stage, you won’t be negotiating terms for loans. Instead, you’ll be learning about which lenders have the most affordable rates so you can make an offer for a house.

Once the Seller Accepts Your Offer

While buyers will be responsible for the bulk of the closing costs, you can negotiate concessions with the seller or credit once you have accepted an offer to purchase the house.The seller might request a title transfer fee or an appraisal fee. Sellers do not have to pay closing costs. Before asking for concessions, ask your agent about the best practices in your area.

After You Get a Loan Estimate

After you accept an offer to buy a house, it is time to get loan estimates from multiple lenders. Once you have received a written estimate of your loan amount, negotiations can begin. Ask loan officers from multiple banks to reduce or eliminate fees.Ask loan officers to recommend other Mortgage Brokers. Negotiating the best deal can take hours or even days, especially if there is more than one Beverly Hills mortgage broker competing for your business. When closing, it can be very cost-effective to speak with loan officers.

Once you’re confident that you have the best deal available, let Mortgage Brokers that you are willing to work with them. The loan officer will normally allow you to lock down a rate. There is no room to negotiate once your rate has been locked in.

How to Improve Your Negotiation Skills

Negotiating well can help increase your chances of getting lower fees. These are just a few ways you can improve your position.Learn From Others

A mortgage broker can help you understand the process of getting a home loan and negotiate your terms. Consider taking a course in homebuyer education before you begin the home-buying process.The CFPB’s website has great information about mortgage interest rates in your area. Compare the current mortgage rates to what Beverly Hills Mortgage Brokers has to offer in your region.

Compare Rates and Fees

Don’t assume that your first lender will offer the lowest mortgage rate. Compare the rates and fees of several lenders to determine if there are other offers that you might be able to take advantage of when you speak with other lenders.Credit Score Improvement

If you’re not eligible for a loan, you may not be allowed to negotiate. If you want lenders to consider your business, you should improve your credit score.To improve your credit score, pay off all outstanding credit card debt. Avoid borrowing money. You can get your credit report corrected for free if you discover errors.

Spend More Time

Negotiating with sellers or mortgage brokers can be time-consuming. Consider taking a vacation day to make the process easier. Negotiating doesn’t require you to be absent from work. You should allow yourself more time between the closing date and your offer.Before finalizing the loan details, mortgage brokers will allow you to negotiate.